Tax refunds are almost 11% smaller this year, early data shows

Tax refunds so far this year are markedly smaller than the same time a year ago, according to the earliest data from the Internal Revenue Service, an outcome that many tax experts were expecting.

The average refund amount was $1,963 as of Feb. 3, down 10.8% from $2,201 the same period last year, the IRS reported. That’s based on nearly 8 million refunds the agency has distributed this year versus 4.33 million refunds disbursed last year. Still, a higher share of taxpayers have received refunds so far this year, with 48% of processed returns getting a refund compared with 33% last year at this time.

While the average amount likely will change as more returns are processed, the early data suggests that the loss of several enhanced pandemic-era tax breaks could mean a smaller, key windfall for many American households.

"I would argue that people's tax refunds are going to be less because of the fact that they are not going to get these special pandemic provisions anymore,” Eric Bronnenkant, head of tax at Betterment, told Yahoo Finance before the figures were released. “Obviously, everyone's situation is unique, but on average refunds are going to be smaller due to less stimulus."

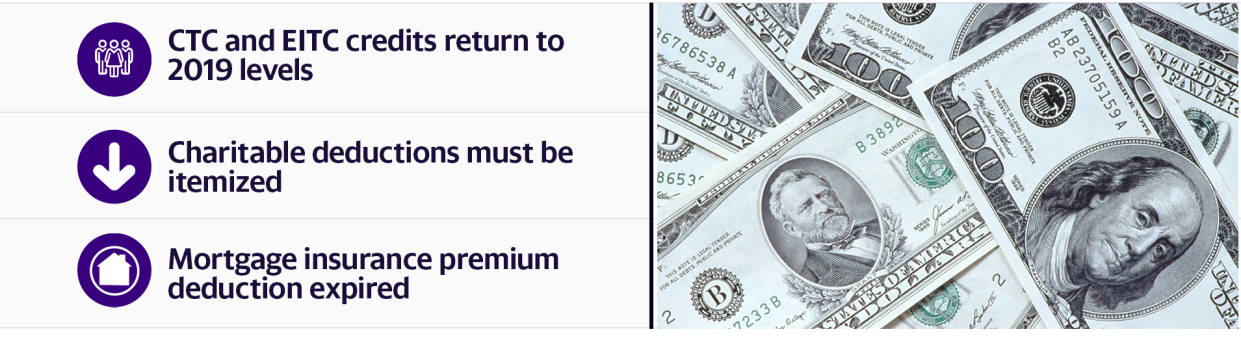

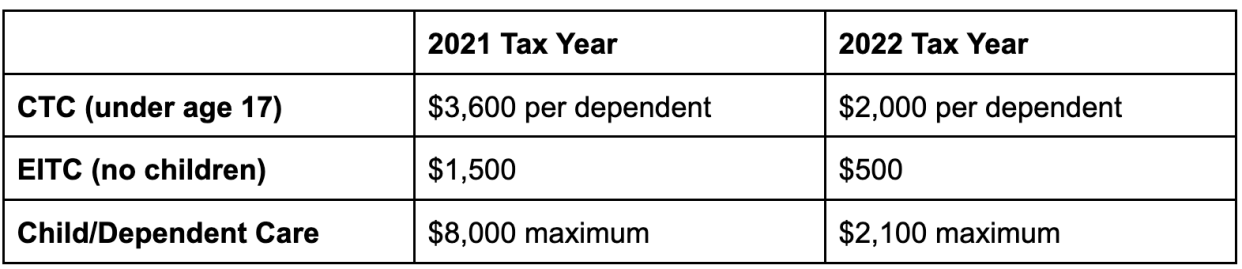

Overall, the average refund last year was $3,293 as of Dec. 28, based on the nearly 110.6 million returns that resulted in a refund, according to the latest data for the 2022 filing season. That was 14.3% higher than in 2021, with the increase largely due to the increased Child Tax Credit (CTC), Earned Income Tax Credit (EITC), and Child and Dependent Care Credit introduced by the American Rescue Act. Those credit amounts have returned to pre-COVID levels.

For instance, the CTC decreased to $2,000 per child dependent versus last tax season’s $3,600. It’s also no longer fully refundable, meaning taxpayers won’t receive the full credit if the amount exceeds how much tax they paid. That hits the lowest-income families the most.

The maximum EITC amount that eligible single filers with no children can qualify for is $500 this season. Last year, these filers got as much as $1,502 for the credit, which also had a higher income threshold then.

Similarly, the Child and Dependent Care Credit — which includes out-of-pocket expenses for child care and day camps — was scaled back this year to $2,100 versus last year’s $8,000.

Other changes, such as the loss of the above-the-line charitable deduction and the expiration of the mortgage insurance premium deduction — also could play a role in lower refunds.

Smaller refunds could be a blow for some households that rely on this lump sum to shore up their financial position. Refunds can make up as much as 30% of a low-income family’s annual income, according to Joanna Ain, associate director of policy at Prosperity Now.

For instance, 46% of Americans said they used their refunds to pad their savings last year, according to a LendingTree survey then, while 37% put them toward paying down debt. More than 1 in 5 taxpayers said they used their refund to pay for necessary household expenses. Much smaller shares of Americans put their refunds toward investing, splurging on unnecessary purchases, or paying for a vacation.

"As we know, tax time is a critically important time for families and individuals — especially low-income households and households of color — and a tax refund can be a lifeline, helping households meet daily needs and start saving for their futures," Ain told Yahoo Finance. "Without the expanded tax credits, it’s not surprising that the average refund amounts are going down. And it’s poor timing—low-income families and individuals are getting hit hard from inflation this year. They need the expanded support now more than ever."

Gabriella Cruz-Martinez contributed to this article.

Ronda is a personal finance senior reporter for Yahoo Finance and attorney with experience in law, insurance, education, and government. Follow her on Twitter @writesronda

Read the latest personal finance trends and news from Yahoo Finance.

Follow Yahoo Finance on Twitter, Instagram, YouTube, Facebook, Flipboard, and LinkedIn

Source: Read Full Article