Bitcoin 2017 Vs. 2021: How This Bull Run Is Different

2021 is shaping up to be a momentous year for Bitcoin as the price hurtles toward $40,000 — more than double its 2017 all-time high. As HODLers rejoice and naysayers are left in disbelief, it’s important to note that a lot has changed in the world since 2017, making this bull run infinitely disparate from the previous one.

Global pandemic and political mayhem aside, many other things have changed in the last few years, even in the microcosm of Bitcoin. In short:

- Bitcoin, not shitcoins

- Accumulation, not trading

- Institutions, not consumers

Bitcoin, Not Shitcoins

In 2017, bitcoin was like a gateway drug for all of crypto. People weren’t necessarily looking at bitcoin as a long-term investment. They were using bitcoin to trade altcoins and get into ICOs — gambling away fortunes in hopes of getting filthy rich.

2017 was the first time that the mainstream public had any sort of exposure to crypto assets and when it happened, it was like the Wild West. Regulation was near zero and anybody, anywhere who had some money could spin up a token and list it on an exchange. Consumer protections were nonexistent and suddenly, everybody was an expert on evaluating early-stage, blockchain-based “investments.”

This led to the ICO craze where everyone from your Uber driver to seasoned Silicon Valley investors became blinded by the hype and got burned on fundamentally unsound investments. To my chagrin, this is likely how the majority of nocoiners today remember bitcoin and crypto. This New York Times article is the epitome of 2017 crypto-mania:

A lot of the hype and money to be made in 2017 was outside of bitcoin, so capital flowed from fiat into bitcoin and then into pretty much every other cryptocurrency. From there, it essentially went to shit, as the creators of the tokens/early investors took everyone’s money by dumping their bags. (Reminder: Satoshi has never sold any bitcoin.) In fact, within the first half of 2018, over 86 percent of all ICOs that listed in 2017 had falled below their initial listing price, and their founders are likely either in jail or enjoying their ill-gotten wealth on a beach in some remote island paradise.

This time, things are different. Money flowing from fiat to bitcoin is staying there. Bitcoin market dominance was at an all-time low during peak crypto mania in 2017 and now, it’s almost double what it was then.

Altcoin volumes are relatively low, especially among retail investors. The people who are dabbling with altcoins, specifically ether, are the ones who are experienced, not newcomers.

Most trading activity in crypto happens in DeFi on the Ethereum blockchain (whale-dominated decentralized exchanges which take technical experience and understanding to use), and in derivatives markets (CME/Bakkt futures and options for institutional players, and offshore derivatives exchanges such as BitMEX).

Bitcoin is no longer being used for trading or as a way to move capital into other crypto assets. Instead, it’s being accumulated for the long term.

Accumulation, Not Trading

In the last two years, over $30 billion dollars worth of bitcoin has been accumulated for the long term. A total of 2.814 million bitcoin are in accumulation addresses right now — that’s 15.16 percent of all bitcoin in circulation.

62.31 percent of all bitcoin in circulation hasn’t been moved in over a year, and less than 15 percent of it is actively traded on exchanges. This much bitcoin hasn’t been HODLed since pre-2017. As you can see, this number plummeted during the bull run when trading altcoins/ICO investing was popular:

People aren’t trading bitcoin, they’re accumulating more and more of it over time and holding it long term (aka, “stacking sats“). This is evident not only through the raw on-chain data and exchange flows, but also through consumer behavior.

People are dollar-cost averaging (DCAing), buying the dip and getting bitcoin-back rewards. Consumer Bitcoin products see this demand, and are building for it:

- Cash App, Rive and Swan DCA: Buy x bitcoin every y time interval

- Ryze Accumulate: Automatically buy the dip and accumulate more bitcoin than by DCAing

- Lolli and Fold: Get bitcoin back on everyday purchases

Why is this shift happening from trading Bitcoin to accumulating it over time?

There are two equally important explanations for this shift:

- The COVID-Induced Macroeconomic Environment

Central banks are printing unlimited amounts of money and interest rates are near or below zero. This will inevitably lead to inflation, so capital is flowing into inflationary hedges such as bitcoin, gold and real estate. Bonds are worthless. Fiat currencies are losing value day by the day. And we’ve already seen two currency collapses in the past year (Turkey’s and Lebanon’s). People are hedging the existing financial system as well as fiat inflation by accumulating bitcoin.

Further reading:

- “Bitcoin As Insurance: Why Investors Know $11,000 Is Just The Beginning”

- “Money Printing, Inflation, And The Bull Case For Bitcoin”

2. Anthropological And Monetary Theory: Evolution Of Bitcoin

All organically-adopted money follows a path of evolution: collectible, store of value, medium of exchange and, finally, unit of account/reserve asset.

Like gold, seashells and beads, bitcoin started as a collectible. Its scarcity, unforgeable costliness of creation and the price somebody else was willing to pay for it are the things that gave it value to the average individual.

Thus, it was heavily traded from 2016 to 2018 as a speculative collectible/commodity, following the same behavioral economics patterns as baseball cards, oil and pork belly futures.

Now, bitcoin is evolving into a store of value — something that will retain its purchasing power, preserving and growing wealth over time. Precious metals, interest-bearing assets, productive land, etc. have been traditional stores of value.

Bitcoin is joining these ranks as consumers, public companies and, most importantly, institutional investors are all buying bitcoin as a store of value in an inflationary environment.

Further Reading:

- “The Bullish Case For Bitcoin”

Institutions, Not Retail

2017’s bull run was led by retail investors — everyday folks trying to get into bitcoin and make money. Smart investors mainly thought it was a scam, with the exception of some notable die-hards like Chamath Palihapitiya and the Winklevoss Twins.

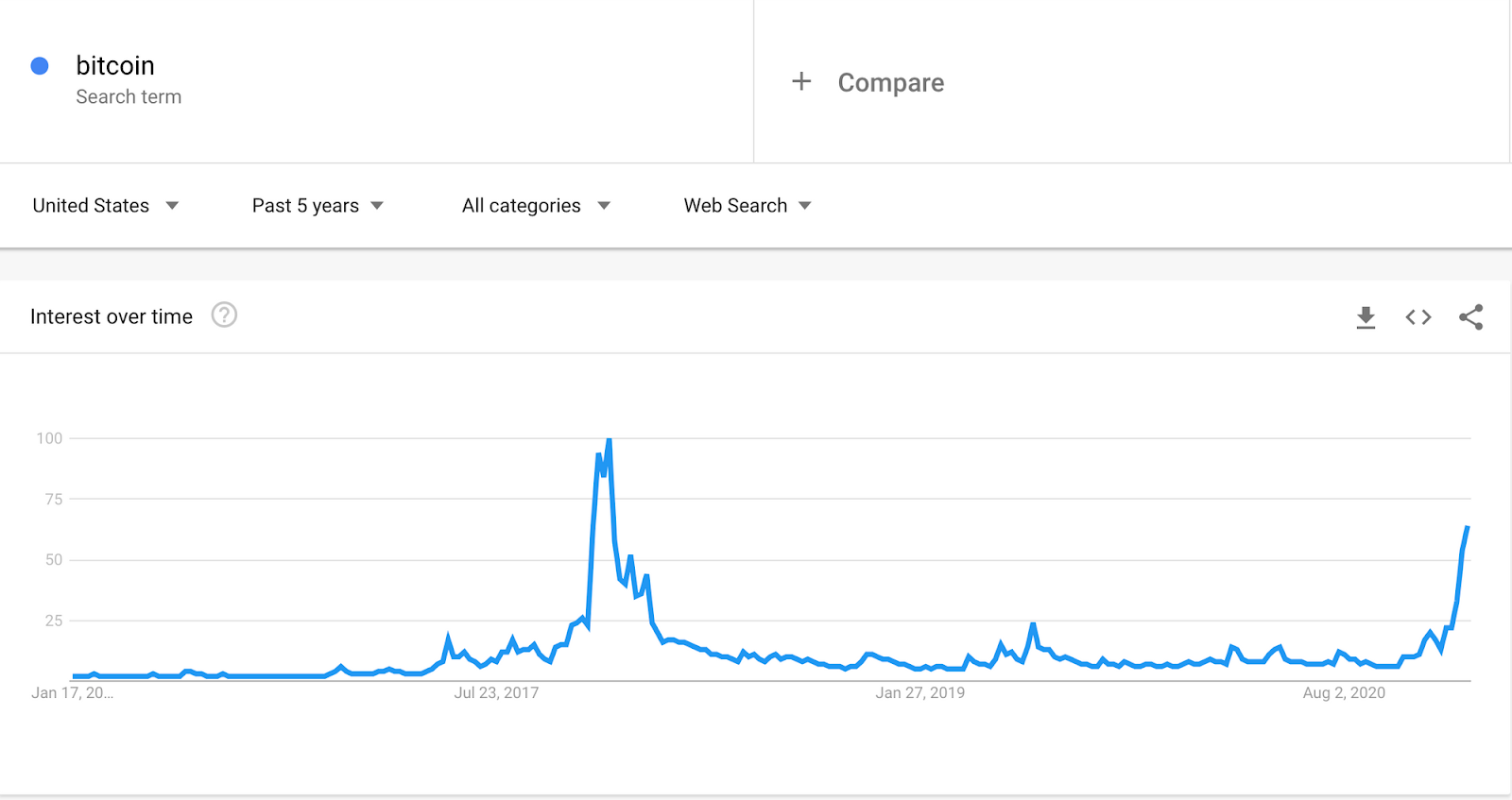

This time, everyday consumers aren’t paying as much attention. Part of that is because every single person is worn out from the dumpster fire that was 2020, and people just don’t care about bitcoin right now. Part of it is the focus from media coverage on pressing issues like COVID-19 vaccines, impeachment 2.0, economic stimulus and more.

With consumers largely preoccupied, institutional investors are leading this 10x rally from $4,000 in March 2020 to new all-time highs past $40,000.

A Fidelity report from June, shortly after unlimited fiscal stimulus was announced, found that more than 35 percent of institutional investors see value in bitcoin, and they’re far less concerned about price volatility and market manipulation than they were before.

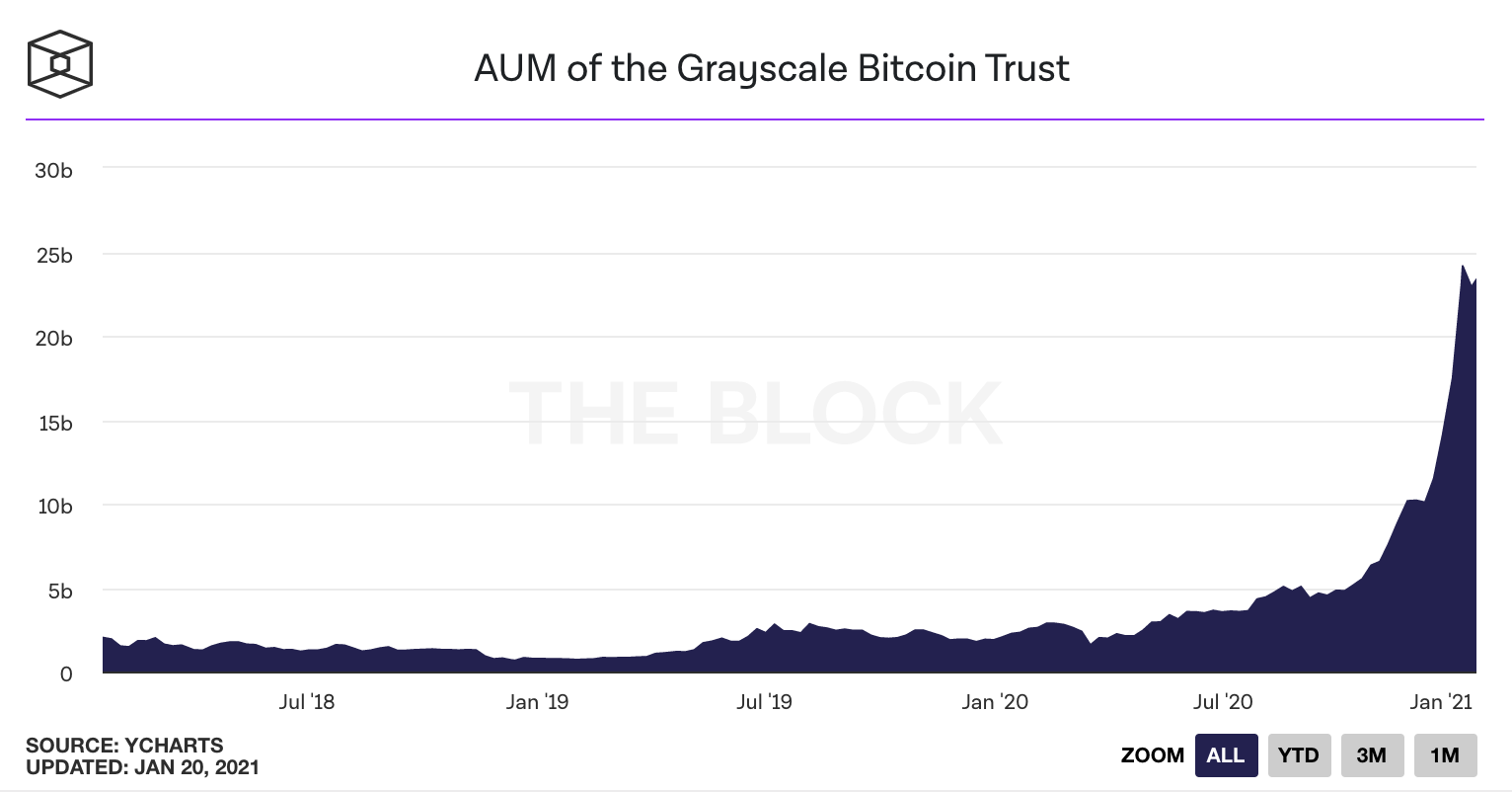

Massive institutional players including JPMorgan Chase & Co., Deutsche Bank, Citibank and Guggenheim Partners have publicly come out in support of bitcoin. Grayscale now owns more than 630,000 bitcoin (3 percent of the total bitcoin supply), mainly on behalf of accredited and institutional investors.

Insurance company MassMutual placed $100 million of its assets in bitcoin. Legendary investors Paul Tudor Jones and Stan Druckenmiller have disclosed personal positions in bitcoin as a store of value. Publicly-traded companies Square and MicroStrategy have placed treasury reserves in Bitcoin, and many more will follow.

Regulatory and infrastructure improvements have made this possible.

In 2017, even if a public company wanted to buy $500 million worth of bitcoin, there wasn’t any easy way to do it, and storing that bitcoin would be an operational and security nightmare. This is no longer the case. MicroStrategy was able to buy about 38,000 bitcoin with minimal slippage and market participants didn’t notice.

Banks can now custody bitcoin, and institutional-grade bitcoin custody solutions have been built since 2017 by companies like Coinbase, Gemini, Fidelity, Anchorage and BitGo, among others. Liquidity providers like B2C2, Genesis Trading and Jump Trading, as well as OTC desks like Cumberland, are all mirroring the order-routing and execution services that exist in traditional markets.

Many of these companies are racing to consolidate these services and build a prime brokerage similar to APEX Clearing for traditional markets and to capture increasing institutional demand.

The increase in institutional investors has legitimized bitcoin for everyday people. Retail interest is starting to spike, but it’s nowhere near where it was in 2017.

Conclusion

The narrative shift from trading to accumulating, combined with the increasing presence of institutional investors, are making this bullish cycle far different from any previous ones in bitcoin’s history.

Bitcoin is no longer a speculative collectible that people gamble on in hopes of making a quick buck — instead, it’s becoming a true store of value alternative to gold that institutions, corporations and consumers are accumulating to protect and grow their wealth over time.

This is a guest post by Abhay Aluri. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Source: Read Full Article