How big will your tax refund be? Changes this year make it harder to guess

This year it could be harder for Americans to gauge how big — or small — their tax refund might be.

With pandemic-era changes gone, many taxpayers might see smaller refunds, especially lower-income families. But an enhanced credit included in last year's Inflation Reduction Act may mean larger ones for a handful. Other developments — such as the expiration of a key tax break for homeowners, crypto investment losses, and life changes — may also affect how big or small a taxpayer's refund could be.

For many Americans, the size of their tax refund is important because it’s often their biggest windfall of the year that they earmark for savings, vacations, debt payments, or even covering basic needs.

“Refunds received at tax time can be an opportunity for many to save, pay down debt, and invest in long-term assets,” Joanna Ain, associate director of policy for nonprofit Prosperity Now, told Yahoo Finance. “They can make up as much as 30% of a low-income family’s annual income.”

American Rescue Plan benefits expired

The average refund last year was $3,176 as of Oct. 28, according to the latest data available from the IRS, up nearly 13% from $2,815 at the end of 2021. The increase was largely due to enhanced credits introduced by the American Rescue Act that have now expired.

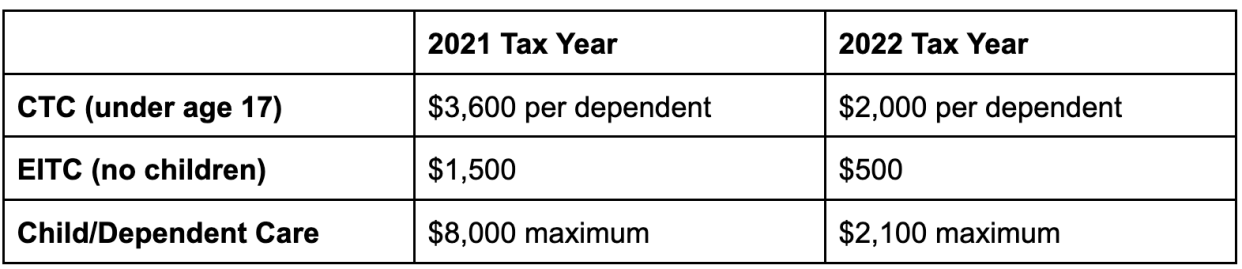

Notably, the Child Tax Credit (CTC), Earned Income Tax Credit (EITC), and the Child and Dependent Care Credit have returned to pre-COVID levels.

The enhanced CTC credit was not extended, so taxpayers can receive only $2,000 per child dependent compared with last tax season’s $3,600. Also unlike last year, it’s not refundable, meaning taxpayers won’t receive the full credit if it’s larger than the tax they owe.

“Since the Child Tax Credit will not be refundable in 2022, many families with lower incomes will be cut out of the credit completely,” Ain said. “In other words, the lowest-income families, the families who need it the most, can no longer receive the full credit.”

Others who still qualify for the CTC may actually see a larger refund this year, even though the credit is worth less. That's because the advanced payments for the CTC have also disappeared.

“Since there are no longer monthly payments, folks could see a larger refund amount at tax time because the entire Child Tax Credit portion of 2022 will come in one lump sum during tax season," Ain said, "rather than being delivered monthly for six months—as it was in 2021."

Last year, the EITC income threshold was also increased for single filers with no children, with many receiving as much as $1,502 for the credit. That expanded credit was not extended, so eligible single filers with no children qualify for a maximum of $500 under the EITC this tax season.

Similarly, the Child and Dependent Care Credit — which includes out-of-pocket expenses for child care and day camps — also was scaled back for this year. Last year, the credit was worth $8,000 for one dependent. This tax season, it’s $2,100.

Other pandemic-era tax breaks went away

Because many nonprofits and charities were impacted by the COVID pandemic, in 2020 the CARES Act allowed single filers and married couples filing jointly to deduct up to $300 in charitable donations without having to itemize their return. Married taxpayers filing separately could deduct up to $150.

In 2021, that above-the-line deduction was expanded even more. Single filers and those married filing separately could get a deduction up to $300, while married couples filing jointly could deduct up to $600.

Taxpayers filing their 2022 tax returns this year, they must itemize using the Schedule A form to deduct any charitable contributions. The above-the-line deduction has been eliminated.

Better tax break in the Inflation Reduction Act

The Inflation Reduction Act (IRA) of 2022 increased the tax credit for solar panels from 26% of the costs to 30% and applies retroactively to panels bought in 2022, with no cap on the credit and no income limitations.

In addition, the act removed the principal residence restriction, meaning that homeowners who installed solar panels on second homes are also eligible. This could increase a refund for homeowners who installed solar panels in 2022.

The act, though, made it a bit harder for drivers to take advantage of the Qualified Plug-in Electric Drive Motor Vehicle Credit. Those who bought a new electric vehicle (EV) last year are eligible for the credit, which is worth a maximum of $7,500 depending on the capacity of the battery.

While this credit could increase a taxpayer’s refund, those who bought the vehicle between August 17, 2022 and December 31, 2022, must show that the vehicle underwent final assembly in North America to qualify. That requirement doesn’t apply to vehicles purchased earlier in 2022 when the act hadn’t been signed.

Mortgage insurance premium deduction expired

Homeowners who pay a mortgage insurance premium (MIP) or for private mortgage insurance (PMI) can no longer deduct this on their itemized taxes. Lenders generally require mortgage insurance as protection in case of default for homeowners who put less than 20% down when purchasing a home.

The deduction — which was enacted under Section 419 of the Tax Relief and Health Care Act of 2006 and extended annually through 2021 — was not renewed for the 2022 tax year and is no longer available for itemization. This may lower a refund for impacted homeowners.

Selling bitcoin or crypto at a loss

If the crypto winter did damage to your digital assets, you can deduct some of those losses if you sold the coins, reducing your taxable income and potentially increasing your tax refund.

Those losses can first be used to offset any capital gains an individual may have. If losses exceed the gains, taxpayers can deduct up to $3,000 in capital losses per tax year against ordinary earned income, such as wages, salaries, and business income.

The IRS also allows taxpayers to carry forward any remaining capital losses indefinitely into the future, with the limit of net $3,000 capital loss per year.

Personal changes

Finally, another reason your tax refund may be bigger or smaller this year depends on your life changes. Getting married or divorced alters your tax-filing status, while having children or taking care of aging parents allows you to take advantage of different credits.

Any time you have a major life event, it’s also important to revisit your paycheck withholdings to make sure enough is being taken out for taxes, so you don’t end up with a smaller-than-expected refund or, worse, owing the IRS next year.

“A little tax planning now can go a long way toward helping you keep more of your money,” Dwight Nakata, a certified financial planner and CPA at YNCPAs, told Yahoo Finance. “Think about changes that happened in your life that may change your tax strategies — like retirement, paying off your mortgage, starting a new business, a new child, divorce, or death in your family.”

Ronda is a personal finance senior reporter for Yahoo Finance and attorney with experience in law, insurance, education, and government. Follow her on Twitter @writesronda

Read the latest personal finance trends and news from Yahoo Finance.

Follow Yahoo Finance on Twitter, Instagram, YouTube, Facebook, Flipboard, and LinkedIn

Gabriella Cruz-Martinez and Rebecca Chen contributed to this article.

Source: Read Full Article